Crypto Tax Gap: Only 49% of Investors Know When to Pay | Coinbase Report

A new report from Coinbase and CoinTracker found that only 49% of U.S. crypto investors correctly understand when their holdings become taxable. With 60% of Coinbase customers missing cost basis data and 4 million 1099-DA forms about to go out, the knowledge gap is about to matter.

Quick Insights

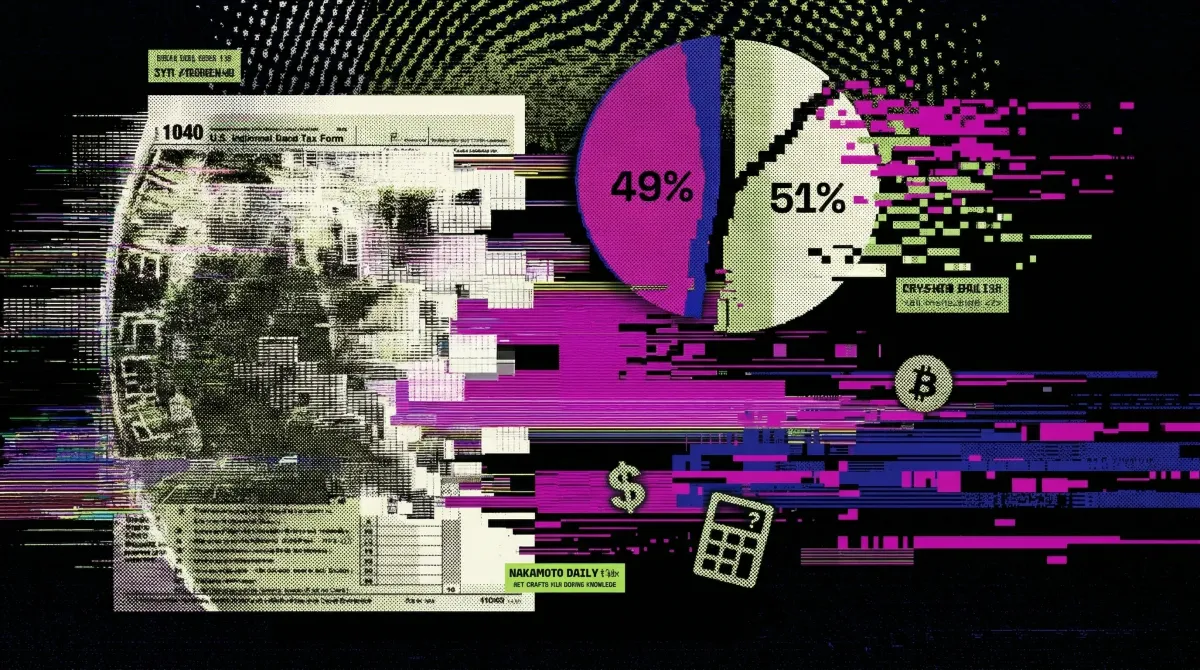

- A Coinbase and CoinTracker survey of 3,000 U.S. crypto users found that only 49% correctly understand crypto is taxable when sold.

- Nearly a quarter of respondents mistakenly believe that simply transferring crypto between wallets triggers a tax event.

- Users averaged 2.5 platforms or wallets each, and 83% use self-custodial wallets, making cost basis tracking significantly harder.

- Coinbase expects to issue over four million 1099-DA forms to customers with under $600 in proceeds.

More than half of U.S. crypto investors do not correctly understand when their holdings become taxable, according to a joint survey from Coinbase and crypto tax platform CoinTracker.

The 2026 Crypto Tax Readiness Report, which surveyed 3,000 U.S. crypto users in late 2025, found that only 49% know that crypto is taxable any time it is sold. Almost a quarter of respondents believe that transferring crypto between their own wallets creates a taxable event, which it does not under current IRS rules.

The findings suggest that even among people who are actively investing in crypto and want to comply with tax law, there is a basic gap in understanding around what counts as a taxable transaction and what doesn't.

Coinbase Says 60% of Customers Have Incomplete Crypto Tax Data

The confusion goes deeper than just knowing when a sale is taxed. The report highlights a widespread issue with cost basis, which is the original purchase price of an asset used to calculate capital gains when it's sold.

Only 35% of respondents said they had ever adjusted their cost basis. That matters because without accurate cost basis data, investors risk overpaying on taxes or underreporting gains.

The nature of how people use crypto makes this harder than it sounds. The average respondent used 2.5 platforms or wallets, and 83% reported using self-custodial wallets. When assets move between exchanges, hot wallets, cold storage, and DeFi protocols, tracking what was bought, when, and at what price becomes genuinely difficult. Coinbase said over 60% of its customers have incomplete cost basis data because of how digital assets move across wallets and platforms.

Every Gas Fee and Stablecoin Payment Is a Taxable Event

The report also points to a structural issue with how crypto tax rules are currently written. Under existing guidance, everyday activities like stablecoin payments and Ethereum gas fees are technically taxable events, even when they generate very little in the way of actual tax revenue.

Coinbase flagged this as a growing concern, particularly in the context of the GENIUS Act, which is designed to encourage stablecoin adoption in the United States. If every stablecoin payment and every small DeFi transaction triggers a reporting obligation, the compliance burden on ordinary users could undermine the goals of the legislation.

The exchange said it expects to issue over four million 1099-DA forms to customers with under $600 of proceeds, illustrating the scale of low-value transactions that will now require formal reporting.

4 Million 1099-DA Forms for Accounts Under $600

The 1099-DA is a new tax form specific to digital assets, modelled on the 1099-B that brokerages have used for traditional securities for years. Its introduction brings crypto reporting into line with stocks and bonds for the first time.

The shift toward standardised reporting is broadly seen as positive for the industry's long-term credibility. Matt Price, director of investigations at blockchain analytics firm Elliptic and a former IRS special agent, described it as a move toward targeted enforcement rather than the broad manual investigations the agency has relied on in the past.

Price has first-hand experience with the complexity of crypto tax reporting. During a previous role at Binance, he was paid partly in crypto and had to do all of his own accounting to file accurately, without a 1099 form to work from.

He acknowledged that cost basis is harder to calculate in crypto than in traditional markets, particularly given the frequency at which many users trade. But he drew a comparison to algorithmic trading on traditional brokerage platforms, noting that similar complexity exists there and the industry has found ways to handle it.

- 49% of U.S. crypto users correctly understand that selling crypto is a taxable event

- Nearly 25% incorrectly believe wallet-to-wallet transfers are taxable

- Average user operates across 2.5 platforms or wallets

- 83% use self-custodial wallets

- Only 35% have ever adjusted their cost basis

- Over 60% of Coinbase customers have incomplete cost basis data

- Coinbase expects to issue 4+ million 1099-DA forms for accounts with under $600 in proceeds

The survey paints a picture of an investor base that is growing more sophisticated in how it uses crypto but remains largely unprepared for the tax reporting requirements that come with it. As the 1099-DA regime rolls out and enforcement tightens, the gap between what users think they owe and what they actually owe is likely to become a much bigger issue.