S&P Puts Its US Treasuries Index On-Chain in Landmark Tokenisation Move

S&P Dow Jones Indices has brought its iBoxx US Treasuries Index on-chain via the Canton Network, backed by Goldman Sachs and Citadel. It's not an investable product. It's benchmark data infrastructure for institutions building on blockchain.

Quick Insights

- S&P Dow Jones Indices has tokenised its iBoxx US Treasuries Index on the Canton Network, a blockchain backed by Goldman Sachs and Citadel.

- The tokenised index is not an investable product. It delivers benchmark pricing and index data on-chain for institutions building digital financial products.

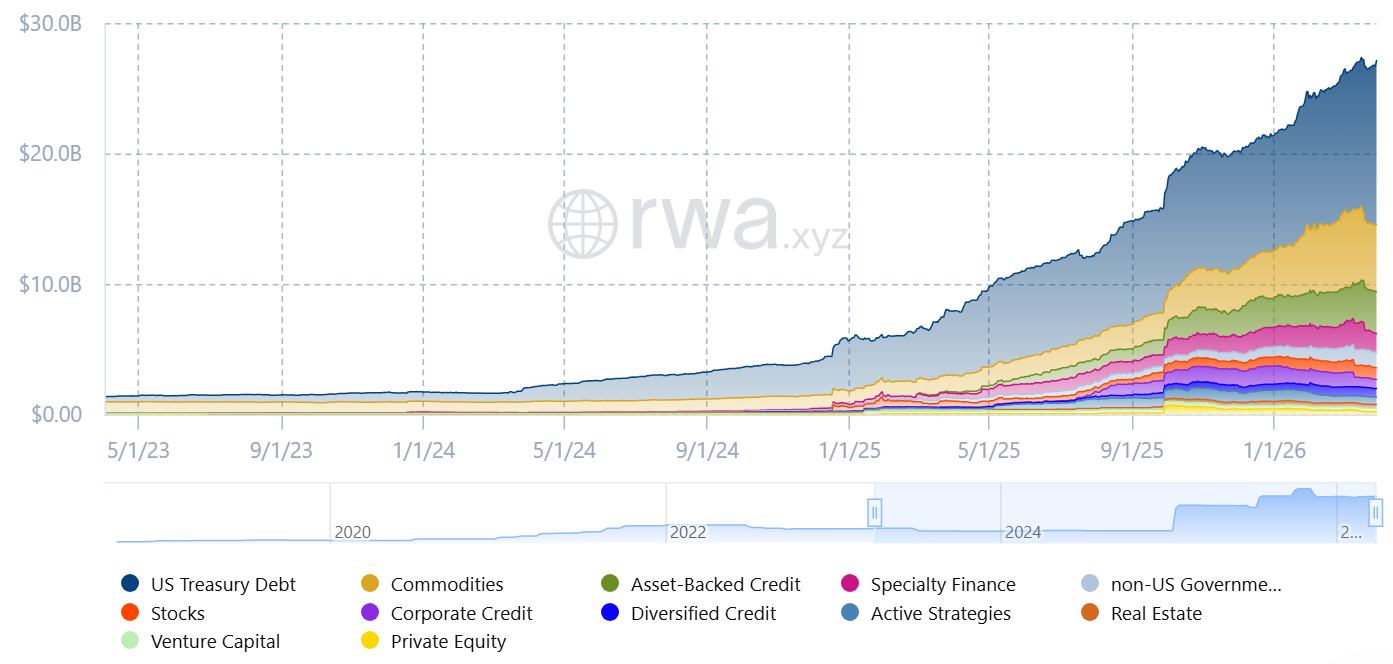

- Over $12.5 billion in US Treasuries have already been tokenised, making government bonds the largest asset class in the $27 billion tokenised asset market.

S&P Dow Jones Indices has brought one of its most widely used fixed-income benchmarks on-chain. The iBoxx US Treasuries Index, which tracks the performance of US government bonds across different maturities, is now accessible as a tokenised data feed on the Canton Network.

The move was announced on Tuesday in partnership with Kaiko, a digital asset data provider that handled the tokenisation and on-chain delivery of the index. S&P retains control over who can access the data, with permissions built into the token itself.

This is not something retail investors can buy. It's infrastructure. The tokenised index is designed for financial institutions that are building blockchain-based products and need real-time access to benchmark data (pricing, index levels, performance metrics) without going through traditional data licensing and distribution channels.

Why S&P Chose US Treasuries as the Starting Point

The decision to tokenise a Treasuries index first wasn't arbitrary. US government bonds are becoming the foundation of on-chain financial systems. They're increasingly used as collateral in digital markets, and institutional activity in tokenised Treasuries has grown faster than any other asset class.

According to RWA.xyz data, more than $12.5 billion in US Treasuries have been tokenised on-chain, making them the largest single category within the broader $27 billion tokenised asset market. BlackRock's BUIDL fund, Franklin Templeton's BENJI, and Ondo Finance's Treasury products have all contributed to that growth.

Putting a major benchmark index on-chain alongside these products means that the data infrastructure is starting to follow the assets. If institutions are going to trade, lend against, and settle tokenised Treasuries on blockchains, they need the reference data to live there too. That's what this does.

Canton Network: Goldman Sachs and Citadel's Institutional Blockchain

The Canton Network is a public blockchain built specifically for institutional use. It has more than 600 participating institutions and validators, and counts Goldman Sachs, Citadel, and several other major financial firms among its backers.

Canton was designed for regulated financial activity, with privacy controls and permissioning that traditional finance requires. Earlier this year, Moody's integrated its credit ratings onto the network, and BitGo expanded its Canton Coin services to include trading and on-chain settlement.

The S&P index tokenisation adds another layer to what Canton is building: a blockchain where institutional-grade financial data and products coexist in the same environment, rather than living in separate systems that need to be bridged.

What This Signals About On-Chain Finance

A data provider like S&P Dow Jones Indices putting a benchmark on-chain is a different kind of signal from a startup tokenising an asset. S&P is one of the most established names in financial data. The iBoxx indices are used by pension funds, sovereign wealth funds, and central banks. When that level of institution starts publishing data natively on a blockchain, it suggests the infrastructure is being taken seriously as a long-term delivery mechanism rather than an experiment.

S&P and Kaiko indicated the approach could be expanded to other indices as demand grows. If that happens, it would mean that the reference data underpinning large parts of fixed income, equities, and commodities markets could eventually be delivered on-chain alongside the tokenised assets themselves.

As we covered in our DTCC tokenisation analysis, the institutions building this infrastructure are not waiting for regulatory clarity to arrive. They're building now, and each integration makes it harder for the industry to reverse course.